At 2:00 p.m., November 28, 2022, the Business School of Central University of Finance and Economics (CUFE) held the 20th Session of the Excellent Academic Forum Lecture Series and the 2nd Session of the Data Science Lecture Series online through Tencent Meeting. Associate professor Zhu Xiaoqian from the School of Economics and Management of the University of Chinese Academy of Sciences was invited as the keynote speaker of this lecture, and more than 20 people (including teachers, master and doctoral students, and undergraduate students) attended this lecture.

Assistant professor Yao Xiao of the Department of Strategics, School of Business presided over this meeting and introduced associate professor Zhu Xiaoqian's resume. Dr. Zhu Xiaoqian is an associate professor and a doctoral supervisor at the School of Economics and Management of the University of Chinese Academy of Sciences. His research interests include financial risk management and big data management decision-making. Besides, he serves as the co-editor of Journal of International Financial Management and Accounting (ABS 2, SSCI), the associate editor of Journal of Operational Risk (ABS 2, SSCI), and the deputy secretary general of the Youth Work Committee and the director of the Risk Management Branch of Chinese Society of Optimization, Overall Planning and Economic Mathematics. He has published more than 30 papers in mainstream journals in China and abroad, e.g. Humanities & Social Sciences Communications, Review of Quantitative Finance & Accounting, Quantitative Finance, International Review of Financial Analysis and China Management Science, and has published one short article in Nature. Some of his achievements have been adopted by multiple government departments and financial institutions. He has obtained 7 software copyrights, applied for 5 national invention patents, won the second prize for a ministerial and provincial-level S&T progress award, 5 best paper awards at international conferences and other awards.

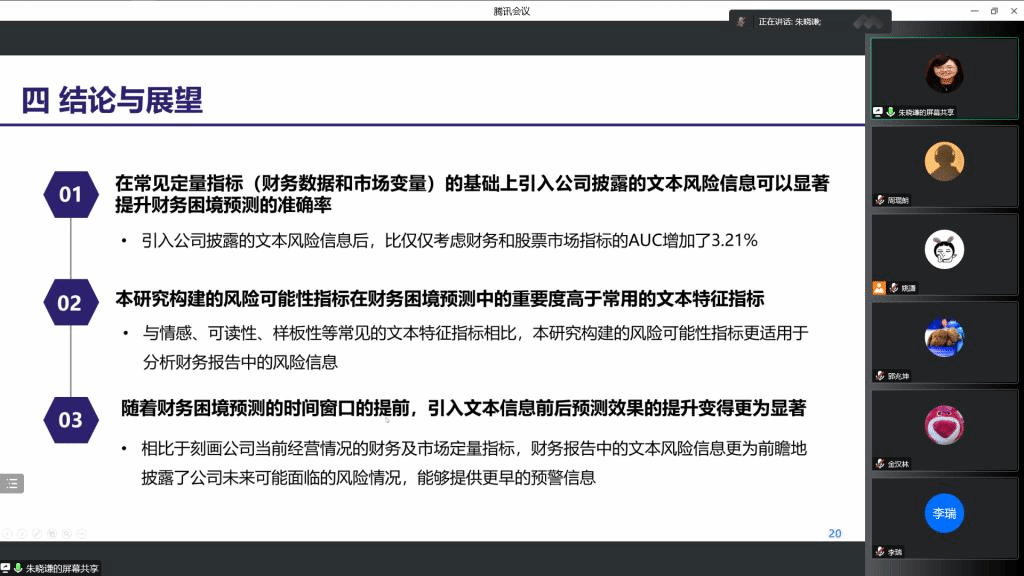

The topic of associate professor Zhu Xiaoqian's lecture is “Research on Financial Distress Prediction Considering Text Risk Information in Financial Reports”. Classical research on financial distress prediction is mostly based on quantitative data such as financial indicators and market indicators. In this research, he innovatively introduces the risk information disclosed in text form in the company's financial reports to conduct financial distress prediction. Besides, he comprehensively mines the key risk information contained in the text from both the expression form and content of the text, and builds a prediction model based on machine learning methods. The empirical results show that integrating textual risk information in financial reports can significantly improve the effect of financial distress prediction of an enterprise. After the report, Dr. Zhu also introduced the contribution information of Journal of International Financial Management and Accounting and Journal of Operational Risk, as well as the special issue information of Emerging Market Review, to help everyone further understand the latest developments of these international journals.

After the sharing, the attending teachers and students actively participated in the discussion about the topic of the lecture delivered by associate professor Zhu Xiaoqian, and the associate professor answered their questions in an enthusiastic manner, further deepening their academic exchanges.

The “Excellent Academic Forum” is an academic exchange platform established by the Business School to fulfill the mission of “contributing new management knowledge”, which focuses on cutting-edge theoretical issues and organizational development dilemmas in the discipline of business administration and the Chinese enterprise management practice, and brings together frontier ideas and innovative ideas in China and abroad, so as to explore Chinese solutions for China's social and economic development.